Intangibly whatever?

I have forgotten which, but a famous book on investing (probably Quality of Earnings) features a story in which the author found a company selling below book value, only to discover that it mostly consisted of a lame radio jingle, which went something like “X is the beer to have when you’re having more than one”.

I probably do not need to remind you that I look at intangible assets with a certain disdain. I am a cheapo investor, hoping that this gives me a little bit of room to be wrong and still end up right. My basic starting point in most things, both within and outside investing, is “you want me to pay WHAT?”

However, having said that, some of my best investments to date have been companies with cheap valuations and essentially zero value pencilled in for intangible assets, despite the quite obvious value of such intangibles. The one that comes most readily to mind is Stanley Gibbons, which is still a major part of my non-Japanese portfolio.

In Japan there are quite a few similar cases of underappreciated intangibles, but it is obviously difficult for non-Japanese investors to understand this kind of value. To be honest, it is even difficult for me in many situations when I have not been to a given prefecture where a company has its stores, for instance.

The following company is an average sports product brand which is not exceptionally stretched on valuation and does arguably offer reasonable safety.

(MM Yen)

Overview numbers

Overview numbers

They have had depreciation running well ahead of capex recently, so you can perhaps add another billion on to get to FCF.

Revs & op inc split

Revs & op inc split

NB: The above op inc numbers do not include 2008, which was much higher.

The company has been growing overseas, doing a particularly good job in the US and Asia/Australia. They say that Asia will now shrink as the Chinese boycott Japanese goods. Interestingly, there was an article in the Nikkei a few weeks ago saying that Japanese brands are doing surprisingly well in China due to their reputation for quality, but the main beneficiaries are folks like food companies and air purifier manufacturers.

This company spent a load of money on the Olympics, and I do not expect there to be any particular catalyst to launch it into mega-profits. Probably the market is also not expecting much of them either, as the share price has gone nowhere for a while. But they are slowly expanding, particularly in US/European shoes.

Mkt cap = 51.8 B Yen

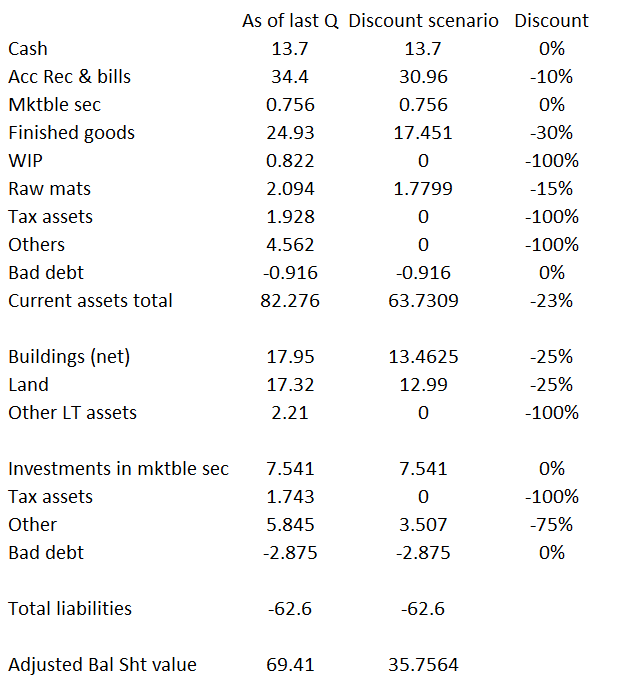

Balance sheet

Balance sheet

Lease obligations are minor.

I cut the buildings and land by 25% because it is difficult to evaluate their real estate. This is due to a. their lumping together some retail and general business assets by geographical area, and b. because the largest asset in there is their HQ building. Although the location is very good – not far from where I used to live – it is risky to assign a large value to a single asset like this. Especially if you are as timid as a squirrel, as I am.

(http://ja.wikipedia.org/wiki/%E3%83%9F%E3%82%BA%E3%83%8E).

HQ

HQ

The big red rectangle is Osaka station, the pointer (C) is Mizuno’s HQ building. Funny how all the foreign analysts are drooling over REITs but no one seems to be yet examining real estate on ordinary company balance sheets …anyway…

They have over 18,000 m2 in mainly second-tier (and some prime retail) Osaka land & buildings, 1,800 m2 in Tokyo, and some elsewhere.

LT investments are mainly shares (c. 80%) and bonds. I left them valued as-is, even though they will be more expensively marked now – same applies for marketable securities in the current assets. “Other” investment assets appear to be some niche trusts set up by the likes of Nomura et al. – no idea what they might really be worth, but probably they are worth something, so a 75% cut should cover it.

That gives us an enterprise value adjusted using my method of around 16B Yen.

The question now becomes, what are we willing to pay for a so-so sports goods company with a bankruptcy value of something like 36B Yen?

If the free cash flow were to stay at something like 3B Yen, then would the current market cap of around 51B Yen make sense? No, I think it would be too low. The reason is because this is a company that will probably grow over time, it has recently been spending a lot of money on advertising (particularly at the 2012 Olympics) and therefore near-term earnings will be depressed, and you should get something for its stability – or, if you prefer, for its brand name or share-of-mind or whatever. The name of the company is Mizuno. I think that to set up this company would probably cost more than 51 – 36 = c. 15 B Yen. Just as a fun fact, Nike spent $2.711 B in FY2012 on what it calls “Demand creation” – basically promotion. ASICS spent 20.755 B Yen.

I do not think that Mizuno is going to suddenly skyrocket here or anything. I just have a sense that it has to be worth, on a net basis, more than what ASICS spends on advertising in one year, and it is fairly safe due to its core business in Japan and its balance sheet. For those not looking at niche micro-caps this is one to consider – they even have English data, it seems. I hold some shares in this company, and would like the market to give me a bit of a discount for me to increase my conviction on this name. Without any fundamental change to the currently-visible earnings picture, I would venture that the business could change hands between reasonable people for something like the 36 B Yen of bankruptcy value plus 10 x 3 B Yen of realistically achievable long-term sustainable FCF (reasonable people can disagree here), and then at least 10 B Yen for the intangible value – pocket change for a name that has been around since 1906. That comes to 75.5 B Yen, which translates into a share price of 46% above where we are now, and just a bit below my target rate of return. Of course, if I am correct that the market is ignoring the potential for any kind of improvement in the near term and if any improvement materializes, then the market is likely to go nuts and assign all kinds of hopes, dreams, and bold predictions and way overshoot a conservative valuation – but I am not counting on that. In fact, the company is a little bit mangy and I would not be surprised if they screwed something up in the short term.

By the way – my sports shoes are ASICS.

{ 8 comments… read them below or add one }

Plus, recognisably Japanese sporty thing makers should get some free growth in their intangible assets if/when the Olympic games come to Tokyo in 2020.

I seem to remember Mizuno being more popular during the 1980s when Japan was doing well and when baseball was more popular (I still have my Mizuno glove). Both baseball and Japan are headed for greater popularity, this could be a social mood play.

Hi,

I think that the Schaefer Beer intangible story was Michael Price’s introduction to Graham’s 1937 Interpretation of Financial Statements.

Recently, I have been looking at a small Japanese software IT company with high returns on invested capital called Toho Systems Sciences 4333:JP. I think that it has an EV/ebit 50%. From what I can understand of its website and financial reports through google translate, it has an alliance with Oracle and helps companies manage their software and IT computer systems. I wondered if you had taken a look at this company.

I keep digging through these low ev/ebit, high roic Japanese companies on the FT.com global screener. I own Toho Systems.

I also came upon BP Castrol 5015:JP. It is another low ev/ebit, high roic Japanese company. It sells motor oil for car engines. It is a subsidiary of BP. I did not buy this company mainly because of the fear that cars become totally electric, and no longer require motor engine oil. I am not sure if this is a reasonable or correct fear. It just has prevented me from buying.

I would be interested in hearing what you think of these companies. I understand if you are too busy to respond. I figured that I would just keep bringing these Japanese companies that I come across to your attention, because you might be interested.

Thanks again for the great articles!

Sincerely,

Hugh

Hugh,

Appologies for never getting back to you on this. Half a year is a long time in the stock market.

In my opinion, in sleepier times you could have justified buying sleepy companies paying decent divs, but in the current market you need to have either pricing power, growth, or some compelling change (“catalyst”, although I hate using that word). The reason why I do not look at roic as a metric per se is that, for instance, my translation company has an roic in the thousands of percent, but that is because we don’t need almost any capital, and I could invest more capital, but that would bring the roic right down (i.e. it would be a waste of money). The fact of having something to put the capital into is important in itself. Many cash-rich businesses just run out of things to invest in, especially in Japan. Sorry if that is not very concrete.

Regards,

Jan

Thanks for responding! I appreciate hearing your thoughts on these matters.

Hi,

I meant to say that I think that Toho Systems has an ev/ebit 50%.

Sincerely,

Hugh

Hi,

I meant to say that I think that Toho Systems has an ev divided by ebit less than 3, and a roic greater than 50 percent.

I hope that it goes through correctly this time. Sorry for the multiple comments.

Sincerely,

Hugh

Hugh – thanks for the comments. I will answer a bunch of questions I have got over the past few days in one or two posts next weekend.

Regards,

Jan