There is nothing to see here – this post is not about Japanese shares.

A few months ago I mentioned that I was considering shorting ABM:LN. This was because of obvious store overexpansion. The stock collapsed a few days ago, and the question now is: is this an attractive risk-reward situation?

I roughly jotted some ideas down and I have nowhere to put them other than this blog for the moment, so I am sharing them here. I will get back on subject (Japan) soon… sorry.

The basic company stats are like this:

(mm GBP)

Mkt cap: 74

NCAV (Curr ass- Tot Liab) = 100 – 65 = 35

|

2008 |

2009 |

2010 |

2011 |

2012 |

|

| Net inc |

7.24 |

11 |

14 |

15 |

16 |

| DD&A |

1.2 |

1.33 |

1.66 |

2.28 |

3.13 |

| Capex |

-1.69 |

-2.29 |

-5.07 |

-8.49 |

-7.95 |

| FCF |

6.75 |

10.04 |

10.59 |

8.79 |

11.18 |

So, in theory at least, you could buy this stock now at around 2.9x trailing FCF.

But looking backwards in this situation is not an opportunity for extrapolation, obviously.

This company, as well as its listed competitor H&T (HAT:LN), have rapidly expanded their “gold purchasing” businesses over the past few years, and getting out of it will be an issue.

“Gold purchasing” is a polite way to say “exploiting poor people”. I do not usually mount a high moral horse in investing, but if you have ever seen poor people in a poor neighborhood handing over their jewelry, then you will naturally wonder what they need to pay for – probably accommodation, utilities, booze, and crack.

I will also leave aside here the discussion on gold itself as a store of value and ultimate collateral for money.

But basically what happened is when the gold price fell, ordinary people (i.e. not futures traders) stopped selling gold and started buying it. This obviously is a problem for the likes of ABM and HAT, because their big expansion programs now probably have to be reversed or redirected. Their gold positions are hedged with put options, btw.

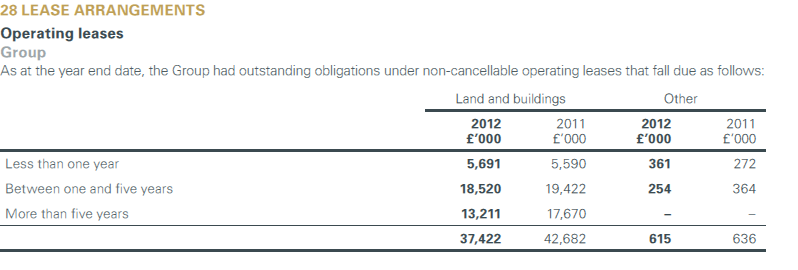

Now if it were just a case of closing down a few stores it would not be such a big deal, but ABM has the following leases:

Op leases ABM

Op leases ABM

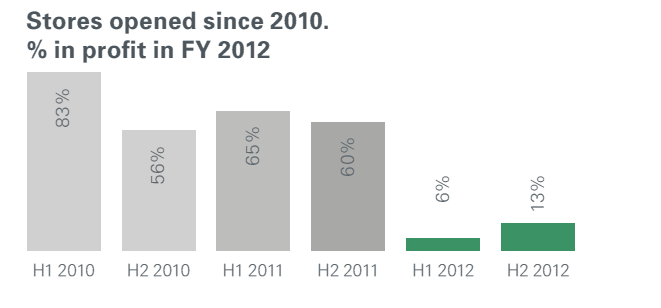

And, more recently-signed leases are the less profitable stores.

We know that because they tell us this:

Store profitability ABM

Store profitability ABM

From the last AR (emphasis added):

38% of our full-line store portfolio has been opened since July 2009 and is immature. On average, the new stores are hitting the profit contribution targets in our five year plan roll out model, assisted by the contribution from Gold Buying. We plan to open 5 stores in FY 2013 compared to our recent run rate of 25 per annum allowing a focus on driving returns from our immature new store portfolio including the introduction of new products and services into the new estate.

They have known for a while that this mad expansion was not a good idea – they even say in their last AR that FY13 gold purchasing will be lower. They knew that if you whack the tree a sufficient number of times, the amount of fruit that comes out will be less. But they still decided to go for short-term profits regardless. I’m not going to judge – ok, sure I am – that was dumb and you are fired.

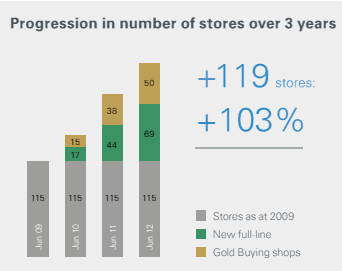

However, the number of dud stores is limited relative to their total store base:

ABM store growth

ABM store growth

Assuming that all the gold-buying stores opened after Jun ’10 are not worth operating, that is 45/234 stores, and it is likely that the dud stores are smaller and have lower rents (more marginal areas) than profitable ones, you could guess that the value of those empty stores would be something like 10% of their lease obligations (i.e. 3.7m GBP).

They currently owe about 50m GBP on a credit line that lasts until Nov 2016, and their current assets do not have a lot of cash. That credit line is up to 65m GBP, and they will surely need to use some cash for restructuring now.

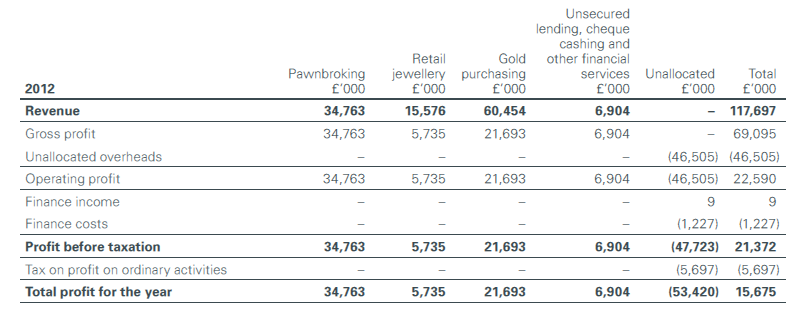

So let’s look at the segments, and take a stab at guessing some numbers:

Their segment reporting is a little strange, since the PBT and operating income numbers are the same (as are the Op Inc and Rev numbers for two segments), and then they have a very large amount of Unallocated costs:

ABM 2012 segments

ABM 2012 segments

…which is pretty unhelpful.

But, at least we can see that gold purchasing operating margins were around 36% – way too high (although the real margins could be lower). HAT’s margins in this business are around 20%, and overall industry margins should collapse (in fact, have already collapsed) as punters have less jewelry to sell (they say this themselves) and there is more competition.

So we punch in some assumptions into a very basic model…and then just play around with some numbers to get a feel for what kind of effects there are:

ABM rough number sandbox

ABM rough number sandbox

The key variables are highlighted in boxes.

In an optimistic scenario, say -10% Unallocated cost reduction, -20% gold purchasing volumes, and gold purchasing margins at 20%, you get a net inc of 11m GBP. Changing to a gold purchasing margin of zero (wiping out the gold purchasing business) and changing cost reductions to -5% gives you about 2.3m GBP of net income.

Of course, there are lots of possible scenarios here, I am not making any bold assumptions with the core business, and in reality they are likely to report some non-recurring costs, but for our purposes the decision to make here are: a. is the gold purchasing business worth anything or is it a liability? And, b. how much can they cut costs?

I think that the answers to these are linked, because if we assign zero value to the gold business long-term, then we need to give them some credit for cutting costs. A zero contribution from gold and 15% cost cutting would be 5.7m GBP. That level of cost-cutting would bring Unallocated costs down to 2011 levels.

And if you consider the likely FCF to come out of this, then you need to take at least a few mGBP out of the net inc for a year or so for store revamps. They will not be able to get out of their leases, so they will need to operate them even at low margins (or close them and eat the losses) – but before they can do that they will probably have to convert some from gold purchasing to jewelry retail or payday loans.

This is the poison of rapid store expansion, and the red flag that signaled a potential short.

There are very limited barriers to entry in gold purchasing, and due to the poor economy and difficulties in borrowing, many poor people were selling their jewelry, leading to a small boom in this business niche. And the fuel for the boom was the gold itself, which is now drying up. Add to that the increasing risks taken on with store expansion in increasingly marginal areas (analogous to drilling smaller and smaller oilfields), and you have a recipe for disaster.

Anyway, the top man just got kicked out, to be replaced by the guy who previously ran things. Is this a comfort? No, not much. The job of cleaning up after overexpansion involves a lot of cost-cutting, but the leases themselves cannot be cut (unless you can get a sub-tenant, which in marginal retail zones is hard), they can only run them off. Also note that the management option minimum strike price is 227p/sh. And consider that it would be rational of them to cut the dividend – but I do not think the market should be unduly surprised by that.

From the interim results:

– Gold buying margins still over 30% (as of Feb 2013)

– Pawnbroking profits up 2.3%

– Retail sales up 16.7%

Read that release: http://www.albemarlebondplc.com/AlbemarleBondCorp/media/A-B/AB-Interim-Results—12-02-2013—Final.pdf

Read the release that caused the crash: http://ww7.global3digital.com/ab/regulatorynews_item.jsp?ric=ABM.L.TK&ref=65129

So back to the question: is this good value here?

The answer, I believe, is that we do not have enough information to say it is a steal. If they would be so kind as to give the market some information about the restructuring that needs to happen, settle the matter of the dividend, and give us some soothing words about rolling over the 65m GBP financing, then we could be more confident in our prognostications.

On a realistic guess at FCF going forwards and normalized for restructuring (say, 4-7m GBP/yr), then it is so-so. You are getting paid to take on the risk of a (somewhat unlikely) liquidity crunch in late 2016, but the basic business of pawnbroking, jewelry retail and unconventional finance is sound, so there should be no difficulty in securing financing from late 2016.

My guess as to the value of the business to a private buyer is 10x (7-4)/2 + NCAV = 10 x 5.5 + 35 = 90m GBP (with 27% error bars) … the mean value in that guess is only 8% above where the stock is trading now.

But bear in mind that a. there are businesses that would love to buy ABM out there (such as 30% shareholder EZ Corp), b. I am very stingy, c. it might not be that bad and the pawnbroking business could grow more.

Lastly, if you have not yet made the connection between this story and the actual gold price, just think for a second what it means that a. average punters don’t have a lot of jewelry to use as collateral/ piggy banks anymore, and b. Mr Joe Average is now buying gold.

{ 0 comments… add one now }