The horse has been incorrectly positioned, in relative terms, and it all boils down to the current account and capital account, which is why the music needs to keep on playing.

Let me explain.

I’m not entirely sure how well the Japanese government has thought all of this through, but their policy of cheapening the yen is causing the trade gap to close quite quickly.

Some Japan trade data

Some Japan trade data

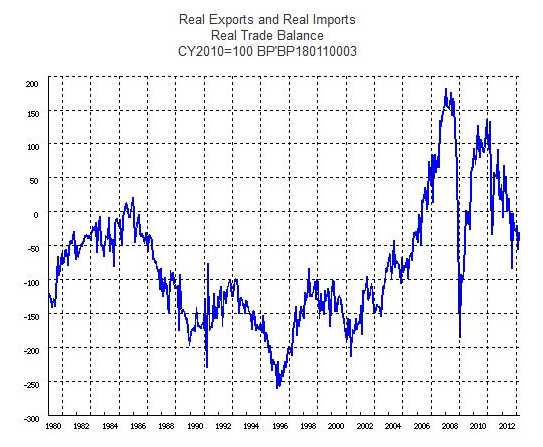

And this is an early sign indicating a reversal of the trade balance deterioration during the strong yen period. You cannot see the effect on this long term chart, but a narrowing trade deficit means that the tendency is for the decline here to slow (and ultimately reverse).

Net trade balance

Net trade balance

The yen has been declining dramatically, and this trade data is over a month old, so presumably the present level of the yen may narrow or even close the negative trade position.

Note that Japan’s current account is already in surplus, as non-tradable flows such as license fees and dividends are a major part.

I believe that this reversal is setting the scene to cause a turnaround in the capital flows that have been associated with the yen decline. This would be significant and, apparently, surprising.

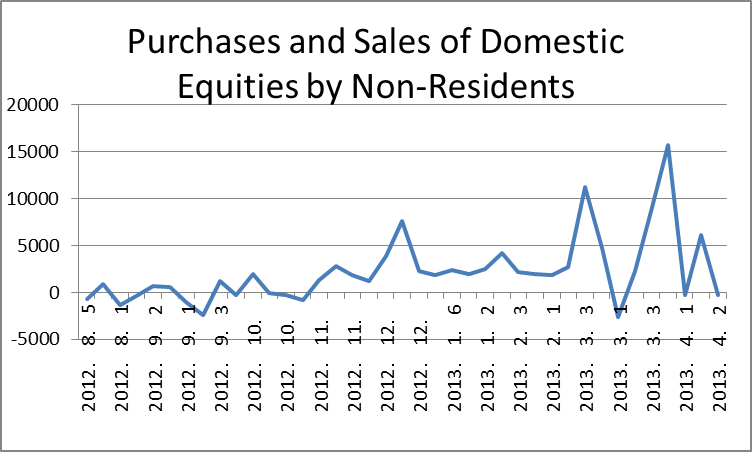

Here is what has been happening to capital flows (units: 100 M Yen). These charts show the flows in/out of Japan for equities, bonds, and money market instruments combined:

Capital flows I – Residents

Capital flows I – Residents

Capital flows II – Non-residents

Capital flows II – Non-residents

Source: http://www.mof.go.jp

Positive numbers are inflows to Japan.

Foreigners have been buying equities, as you can see if you break out the foreigner share purchases.

Capital flows III – Non-residents equities

Capital flows III – Non-residents equities

Japanese institutions have been net sellers to foreigners.

In fact, the selling by Japanese institutions is very high.

So we have an interesting situation whereby foreigners have come in and front-run something (anticipated major capital flows out of Japan) that has not yet happened, in complete disagreement to domestic institutions.

And, if the current account stays positive due to the weak yen, what do you think will happen?

Firstly, putting circular/feedback effects to one side, positive current account inflows ought to cause capital to leave the country, just like for most of Japan’s history. Most of the time, Japan has been a surplus earner and an exporter of capital. This means that its business model has been to import timber, rubber, rocks, oil etc., make it into Sony and Toyota products, sell the profits to depreciate the yen, and use (“export”) the acquired dollars to buy US government debt. The difference nowadays is that those financial flows (not tradable products) are big and constantly streaming into Japan. (Remember that the current account and capital account have to balance.)

If you did not understand that, what I am saying is: it is not different this time, and Japan will go back to its old ways if you give it a cheap currency with no structural reform.

The government wants to stop deflation by weakening the yen and causing an inflation mindset. But there is a real risk that they will screw it up due to causing a trade surplus.

It seems to me that the horse has been allocated somewhat toward the rear end of the carriage.

You see, in the US, UK, and other debtor nations, the debt is fine as long as kindly obliging countries like Korea, Japan, and China are willing to lend you the money and cheapen their own currencies for the privilege of continuing to do so. But Japan cannot borrow money from other countries in any serious amount. Firstly, the interest rates would be so high that the banks would all collapse (or hobble along under fake accounting, pretending that they are fine but being super-zombies), and secondly, Japan’s unwritten rule, since like forever, has been that she shall not be dependent on foreigners for funding (nor for much else other than minerals and cheese), unless said foreigners demolish all her productive capacity with bomber aircraft.

This is a bit of an issue for best-laid plans, as the lack of overseas debt financing as an option means that current account surpluses will be maintained again, and this may undermine the whole Abe program.

The causes of deflation are argued over, but it is broadly accepted that deflation is linked to a high yen, and a high yen is worse during “risk off” periods in the global markets. This is because, during such periods, Japanese investors do not want to invest overseas, leaving incoming capital piling up inside the country and causing demand for yen to be relatively high (as money in other currencies still needs to be converted to yen due to financial flows, while there is less yen being sent outside the country for investment), and thereby deflation.

When we have a deficit in the current account (mainly due to selling less Toyotas), then it is somewhat easy to cause the currency to fall. But when we don’t, then it isn’t.

Therefore, now that the country’s current account surplus has gone up again, the yen will be at the mercy of capital flows, which means the next time the highly frothy equity markets go down, the yen is likely to go up a lot. Add to that the fact that there is a lot of yen shorting by speculators and you have the potential for a nasty sharp unwind unless the music, which sounds like that of a horror movie to me, keeps playing. As an indicator, the short yen position on the Comex amongst small speculators is the largest ever (I think), and amongst large ones it is the highest since around 2007, when the carry trade was popular.

Let me be clear – this is not to say that a current account surplus equals a strong yen, just that it narrows the possibilities. It means that there need to be capital outflows for the yen to not strengthen.

The risks to my view are as follows:

Risk 1. Japanese investors may start sending capital overseas. Ok – where? Bonds are expensive everywhere, stocks overall are a joke*, and everything has been made more expensive when viewed from this side due to the depreciation – are you surprised that capital has been staying at home? But it is still a risk, as it is difficult to say how investors will react if the yen keeps on falling. If it does, and if they do decide to stampede out, then the yen may well crash, but eventually the current account surplus will bring it back.

*On the subject of Japanese equities themselves, I cannot look at any more crap about “still attractive” for 15-20x earnings and 2x BV for companies with Japanese “governance” and competitive positions dependent on the weak yen … makes me sick

Risk 2. Global interest rates rise due to a strong economy. But as I have argued before: A ha ha ha ha ha! A ha ha ha ha ha! A ha ha ha ha ha!

Now, why is this cart behind the horse?

Simply because the government wants to cure deflation by getting the yen to fall, but in the long-term the currency is a symptom, not an underlying cause. They want to get the yen down, increase wealth, and cause increased spending. But it should be the other way around, namely:

Improve economy structurally => More productivity => More income => More spending => Less deflation

This is the backwards way they have it:

Devalue yen => Change inflation expectations => More spending => Less deflation => More prosperity => Structural economic improvements

If every country could get rich by devaluation…

I may be wrong as to their thinking, because government bamboozles me, and I have left out the fiscal part because we are mainly here talking about the yen, but on that I will just say that Japan does not lack for investment capital, just productive investment opportunities given the communist nature of everything in the economy.

As I have argued before, the yen can fall, but increased surpluses will be a brake on inflation (and on the yen falling). Not only that, but it seems that the “Change expectations” part is only working by squeezing household budgets, not in a positive way (unless you work for Nomura/ a Ferrari showroom).

Back to the near term, I am not going to say that the yen will now turn around on a sixpence, but I will say that the setup is ready for a big increase in the price of the yen vs. the dollar as soon as the capital flows move in the way that they usually do in an equity downdraft. Except this time I expect the move could mainly consist of foreigners bailing out of their speculative positions.

Is that enlightening? Probably not much. All this says is “watch out”. And for the record, I am taking the side of the domestic institutions in the argument while also keeping quite a high exposure to conservatively-valued Japanese stocks.

{ 0 comments… add one now }